Legally Separated: How to Prepare Financially

Being legally separated from your spouse is different from being divorced in one big way — legally, you're still married. However, similar to divorce, there are financial issues to contend with, and managing them well is important to your financial security.

Reasons for Legal Separation

According to the American Bar Association, legal separation allows a couple to live separately and formalize their arrangement by a court order or written agreement. Some people opt for legal separation over divorce for religious reasons or because they are hoping to reconcile in the future.

It's important to consider how separation affects different aspects of your life. A spouse can qualify for the other's Social Security benefits if the marriage lasts at least 10 years. Likewise, some health insurance plans will continue to cover a spouse after being legally separated.

Regardless of the reasons for choosing legal separation, many couples will want to live as individuals and untangle their financial knot. Make sure you do the proper research, though, as there are many factors to consider.

Location Matters

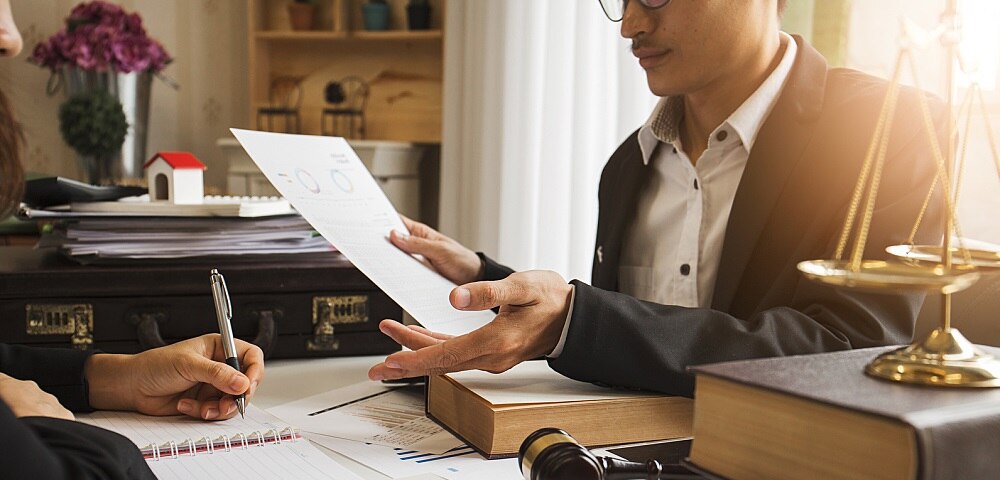

Not all states recognize legal separation, but even in the majority of states that do, laws vary considerably. It's a good idea to consult with a financial advisor and a family attorney to help you understand your financial choices regarding your assets and liabilities.

In addition, a tax expert can help you work through tax implications such as how to file — Single, Married Filing Jointly, Married Filing Separately, or Head of Household.

According to the IRS, you're considered unmarried for the whole year if "you have obtained a final decree of divorce or separate maintenance by the last day of your tax year. You must follow your state law to determine if you are divorced or legally separated."

Setting the Terms

It's a good idea to create a legal separation agreement, even if it's not required. This will define the terms of the separation in writing — including how you will address financial interests.

The document could spell out how you will manage jointly held debts like a mortgage. For example, you'll want to know if both spouses will pay off the loan or will it be just one? If it's the latter, it's worth considering options to remove the name of the person who will not be paying down the debt — any missing payments can affect the credit of both borrowers. Refinancing could be one solution.

The agreement could also outline factors like how to divide the money in joint bank and brokerage accounts, as well as who will live in the family home and pay the expenses. It could also specify how insurance, spousal support, and child support will be handled.

The Legal Assistance for Military Personnel can help you work through some of the considerations you'll need to make. Oftentimes, spouses will hire a lawyer to help with these complex agreements.

If divorce is the next stop, having terms in place that help work through potentially thorny financial issues can help reduce what may be a stressful situation.